America's financial infrastructure was never built for community institutions.

Keystone OS pools loans from community banks, MDIs, and CDFIs into rated bonds that institutional investors can buy. The infrastructure has not existed at this tier for 40 years. We are building it.

The bottleneck was never credit quality.

Securitization is the engine that recycles credit through the economy. Large banks have it. The 4,500 U.S. community banks, the 142 federally certified Minority Depository Institutions, and the roughly 1,400 CDFIs do not. The result is $1.2 trillion of trapped lending capacity sitting on community bank balance sheets while underserved borrowers are told the bank ran out of room.

$1.2 trillion of trapped capacity. Zero infrastructure to release it.

The Federal Reserve Bank of New York documented in 2024 that CDFIs originated $67 billion in loans in 2022, yet just 10 CDFIs accounted for 75 percent of all loan sales. Institutional investors require minimum pool sizes of $50–$100 million. The typical CDFI pool is $5 million. Until that mismatch is resolved, the asset class does not exist.

Keystone OS sits at the convergence of eight layers.

The product surface that ships first is securitization. The platform is designed to extend across every adjacent function the same institutions need.

Five surfaces. One operating system.

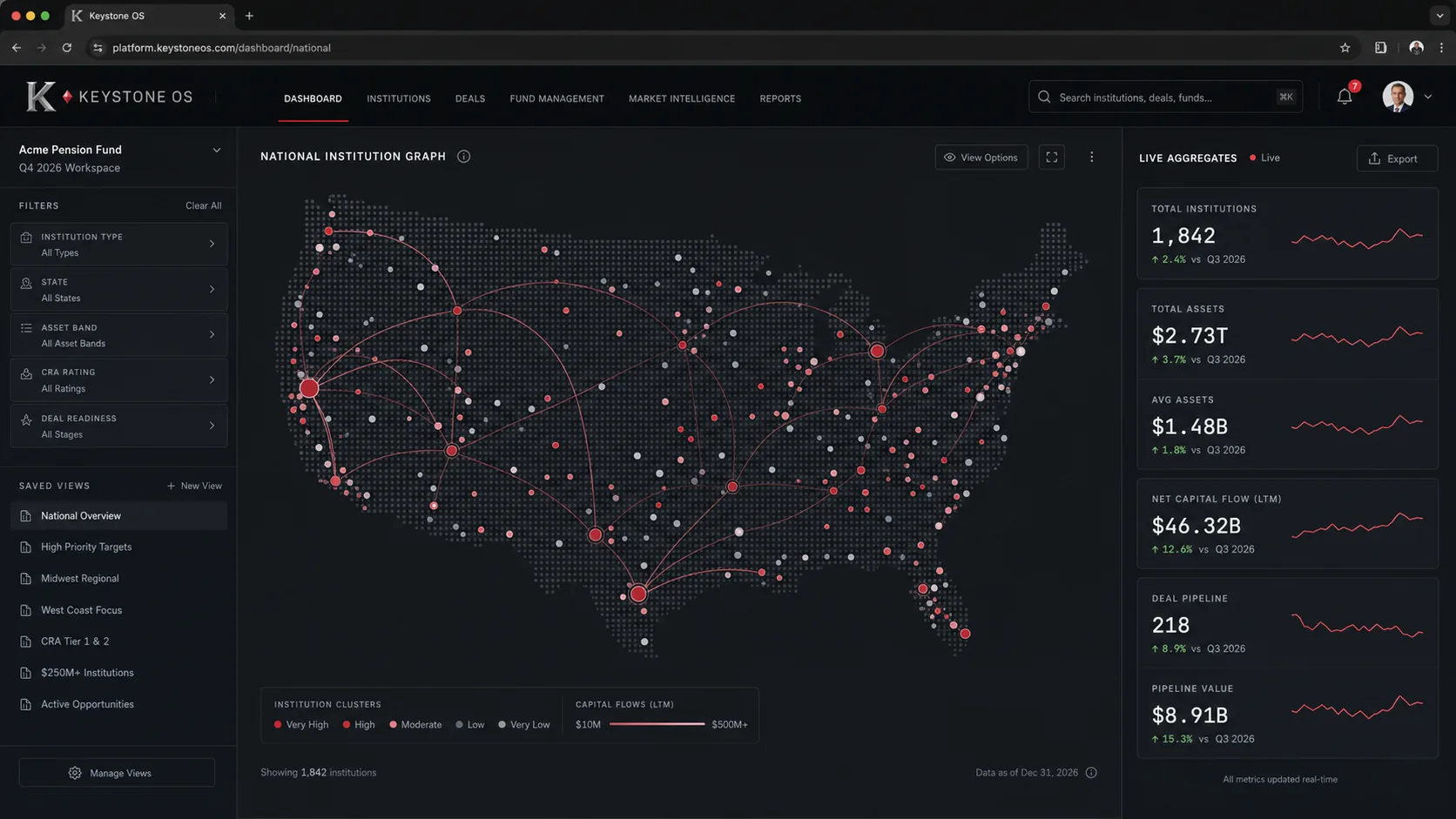

National Dashboard

Every community institution in one map. Every loan tape in one schema.

The entry point for issuers, investors, and analysts. The U.S. map renders 6,000+ institutions as nodes, colored by type and sized by total assets. Filters surface peer sets; a live aggregate panel surfaces normalized loan volume, pool composition time, and deals in flight.

Issuer filters to a peer set, identifies five candidate co-pool partners, and exports a starter pool definition into the Pool Composer.

No competitor has a national institution graph. The data network effect compounds from day one.

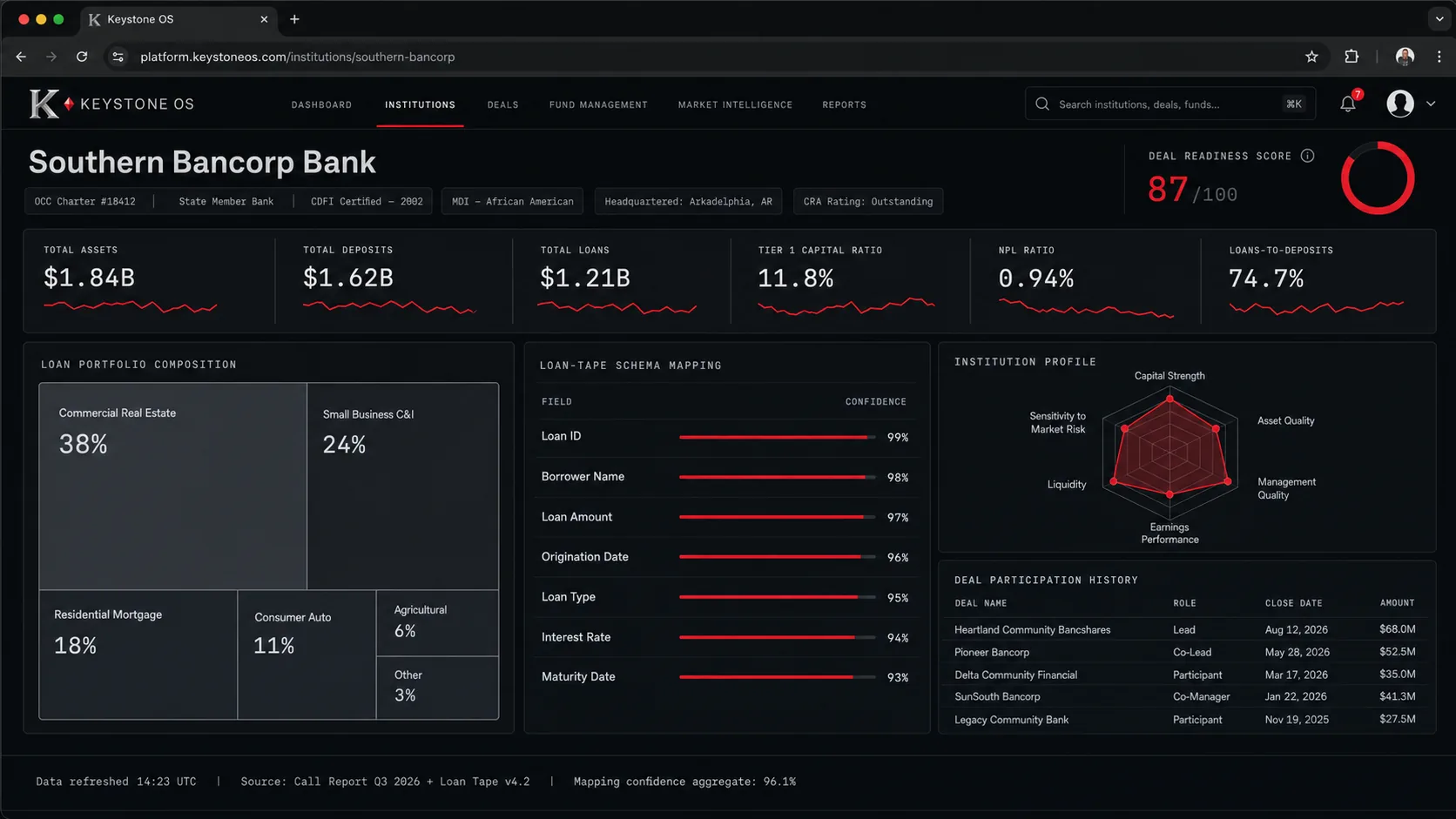

Institution Profile

Every bank, MDI, and CDFI, modeled as a first-class object.

The canonical view of one institution: charter, regulator, assets, capital ratios, CRA rating, and certification status — plus a loan-tape preview mapped into Keystone's canonical schema with a confidence score per field.

Analyst reviews schema mapping confidence, approves low-confidence flags raised by the AI, and signs the institution off as deal-ready.

This is the moat. Once an institution is mapped, it stays mapped — every addition multiplies the value of the graph.

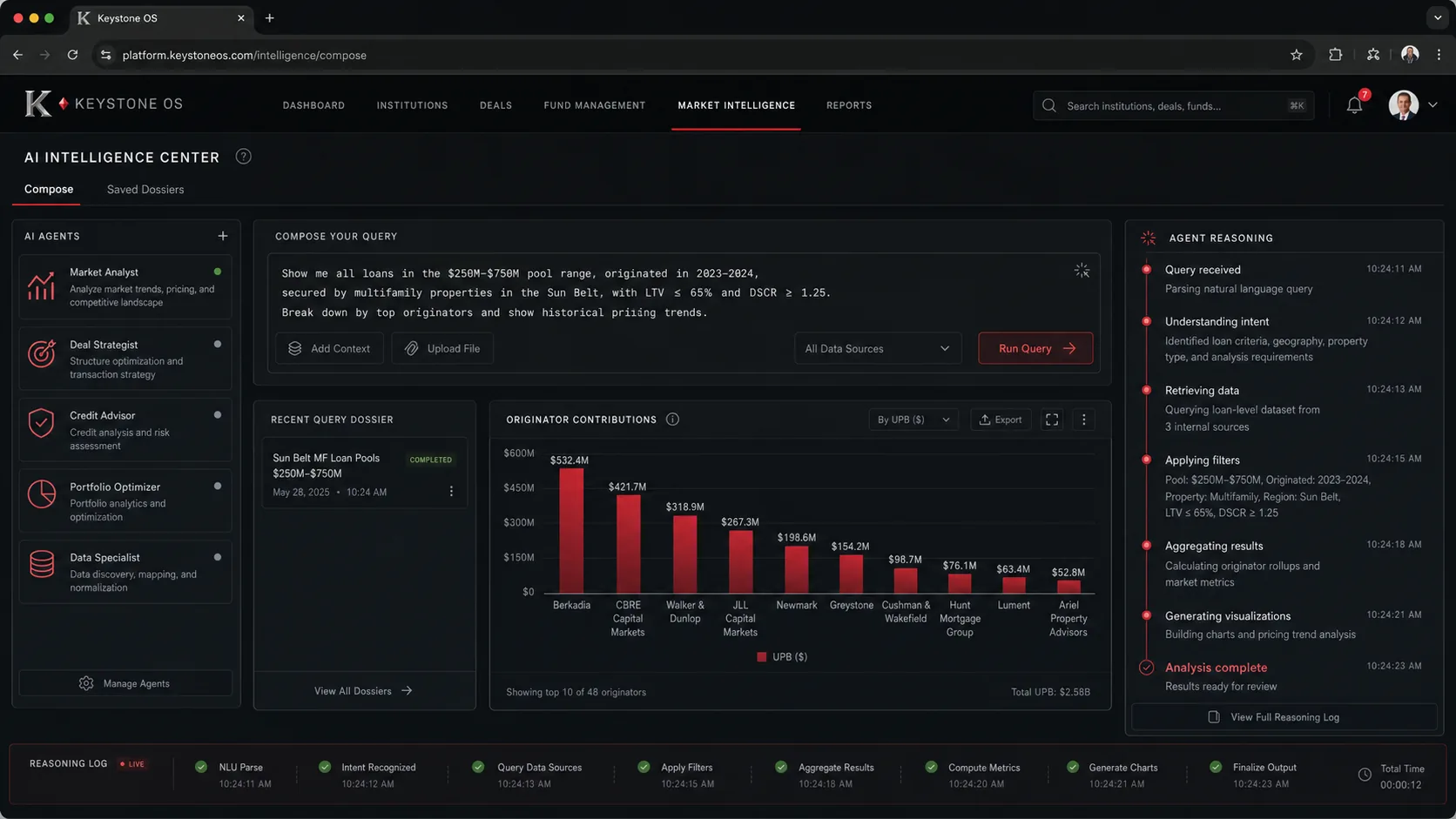

AI Intelligence Center

Six agents. One coordinator. End-to-end deal composition.

The operator's console. A horizontal agent rail shows Originate, Underwrite, Pool, Structure, Place, and Reinvest with live status. A natural-language query bar drives a workspace canvas; the right rail streams SHAP-style reasoning traces in real time.

Operator requests a $50M auto-loan pool from Southeast CDFI originators with no single-bank concentration above 20%. Agents return a candidate pool in under 60 seconds.

The category nobody else has built: AI-native securitization at the community bank tier.

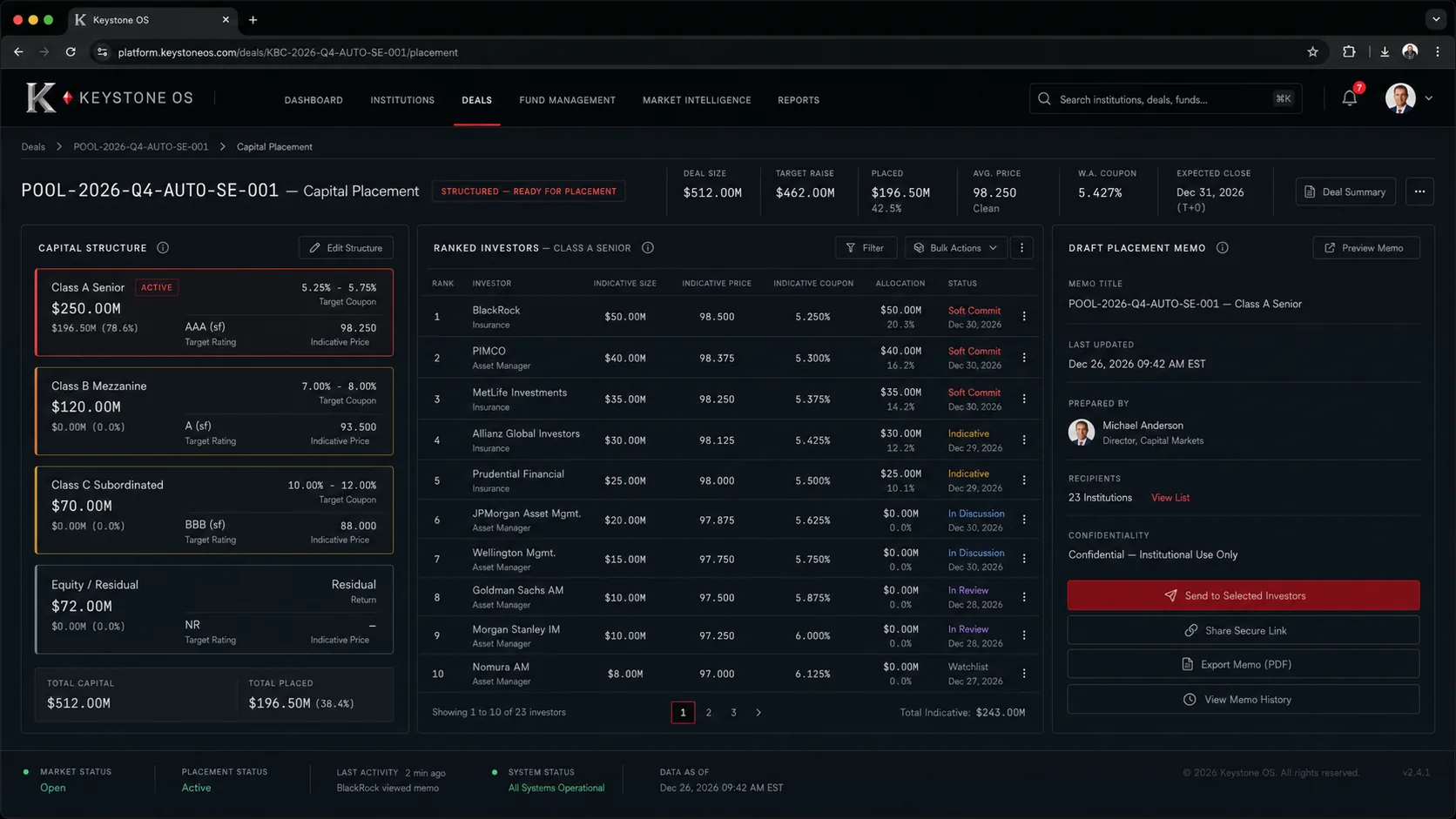

Capital Match Engine

Match every tranche to its right investor.

Sits between Structure and Place. Once a tranche stack exists, the engine ranks every CRA-motivated bank, pension, insurance, and impact fund against tranche characteristics, then drafts a placement memo for the top match.

Operator picks Tranche A, sees the top 12 ranked investors, selects three to approach, triggers draft placement memos, and sends.

The CRA Modernization Rule created the demand. This is the engine that routes it.

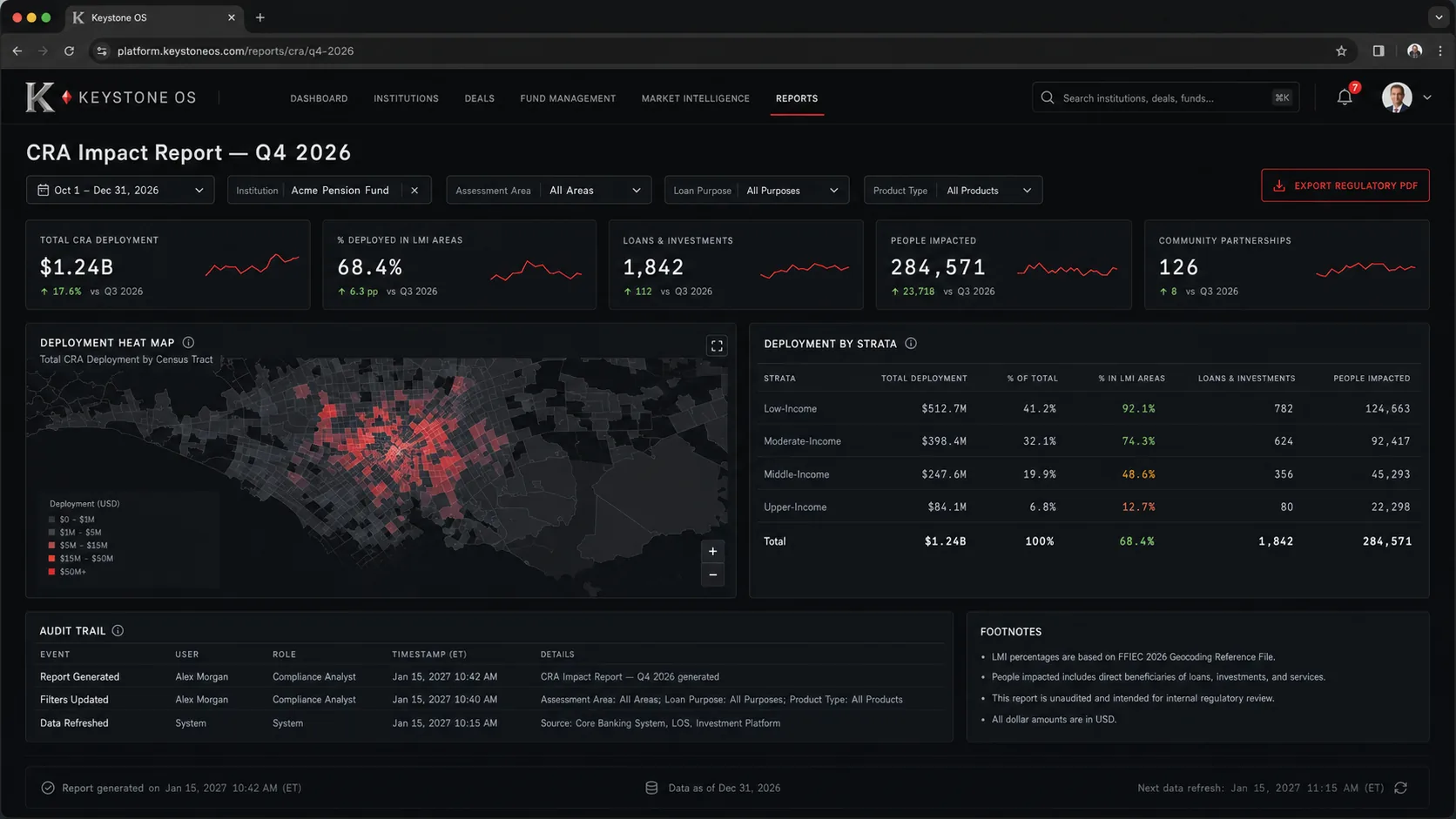

Impact Reporting

Every dollar attributed. Every beneficiary measured.

Closes the loop. Every underlying loan carries originator type, geography, demographic indicators, and sector. Deployment renders by state, by census-tract LMI status, and by borrower type — in regulatory format.

A reporting officer pulls the Q3 CRA report; it renders in under five seconds with a full audit trail.

Without impact attribution there is no CRA premium. Without the CRA premium the asset class never breaks out.

Six agents. One trust. One bond.

Originate

Ingests and normalizes loan tapes across bank cores

Underwrite

Scores loan-level eligibility with traceable attribution

Pool

Composes multi-seller pools to target concentration limits

Structure

Builds the tranche waterfall and credit enhancement

Place

Matches tranches to mandate-aligned investors

Reinvest

Recycles freed capacity back to originators

Two waves converged in 2024. The window opened.

The case is built on public record.

"Pooling and securitizing loans to expand CDFIs' access to capital markets."

"It would be necessary to aggregate loans from multiple originators; one solution might be for a third party to step in."

"The number one need identified by CDFI MDIs was access to capital."

"An intermediary savvy with the expectations of commercial investors while also aligned with the social mission of CDFIs."

"Regulatory actions have entrenched the dominant position of the largest banks while erecting barriers to entry."

"For many of these products there is no secondary market that can unlock capacity."

"Smaller lenders face disproportionate fixed costs accessing secondary markets."

"Pool diversification across originators materially reduces idiosyncratic credit risk."

Built for the regulated environment from day one.

Role-based access control with audit logging on every state change

End-to-end encryption — TLS 1.3 in transit, AES-256 at rest

Immutable audit trails on every loan-level decision

SHAP-traceable underwriting decisions for rating agency review

SOC 2 Type II compliance pathway scoped, in progress

True-sale opinion architecture for SPV formation

Public phase status.

Research complete

Architecture documented, evidence base assembled

Prototype

Schema mapper, underwriting agent, pool optimizer

Regulatory alignment

Rating agency pre-engagement, SPV structure validation

Pilot partners

MDI/CDFI letters of intent

Beta

First synthetic deal end-to-end on real anonymized data

National launch

First rated deal closes (target 2027)

The institutions agree.

Pooling and securitizing loans to expand CDFIs' access to capital markets.

It would be necessary to aggregate loans from multiple originators; one solution might be for a third party to step in.

The number one need identified by CDFI MDIs was access to capital.

An intermediary savvy with the expectations of commercial investors while also aligned with the social mission of CDFIs.

Regulatory actions have entrenched the dominant position of the largest banks while erecting barriers to entry.

For many of these products there is no secondary market that can unlock capacity.

The beginning of a serious conversation.

Join the founding cohort

Keystone OS opens to a closed cohort of institutions and capital partners ahead of public availability. Request a position in the queue. We respond to every qualified inquiry within 72 hours.

For community banks, MDIs, CDFIs, and credit unions.

Originate loans the way you always have. Keystone OS pools, structures, and places them in the capital markets on your behalf. Founding cohort institutions receive priority onboarding, fee waivers on the first pool, and a seat in the product council.

For institutional investors, family offices, and impact-aligned capital.

Keystone OS structures rated, CRA-eligible bonds backed by diversified community loan pools. Founding cohort investors receive first-look access to inaugural tranches, full deal documentation, and a direct line to the structuring team.

Building the infrastructure behind community capital.

The next generation of financial infrastructure begins with visibility, intelligence, and connection.